European agri-food: sectoral contrasts in the face of trade liberalization

In discussions surrounding international trade agreements, European agriculture is often portrayed as a homogeneous sector, unable to compete on the global stage. This oversimplified perception fuels ongoing debates over market liberalization, foreign competition, and the safeguarding of domestic industries.

By Charlotte Emlinger, Houssein Guimbard

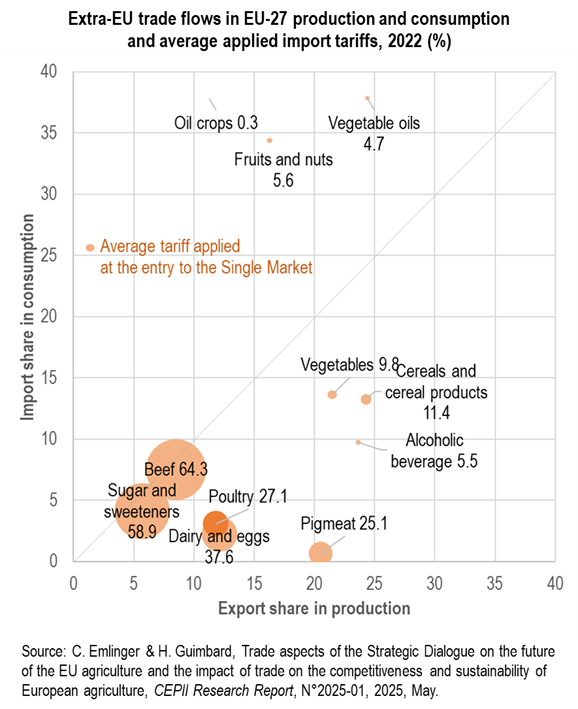

Yet, a closer look at the share of trade in agricultural production and consumption reveals a far more complex picture. Certain sectors—such as cereals, alcoholic beverages, pork, and dairy—export a substantial share of their output (up to 30%), reflecting a proactive and competitive stance. In contrast, other segments like fruit, vegetable oils, and oilseeds rely heavily on imports, which can account for more than a third of domestic consumption.

These imbalances are further accentuated by highly variable and consistent tariff protections: customs duties range from as low as 0.3% for oilseeds to nearly 60% for sugar and beef—sectors that appear particularly sensitive to market liberalization. European agriculture, therefore, emerges as a diverse and fragmented landscape, shaped by conflicting commercial dynamics across exporting, importing, and protected sectors.

< Back