The "new silk roads": an evaluation essay

(2/4): The Belt, Corridors and roads

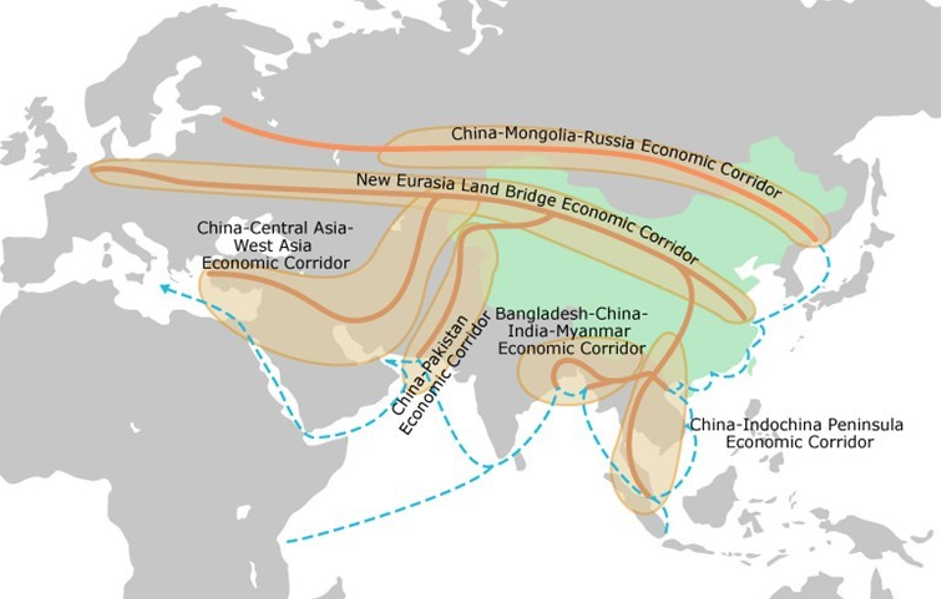

The Eurasian Belt is made of three roads:

- The most used one starts in China (Chengdu, Chongqing, Wuhan...), runs across Kazakhstan, Russia, Belarus and Poland and ends in Northern Europe (Duisburg) with extensions to other European cities (Lyon in France).

- A second crosses Mongolia and joins the Transsiberian.

- A third crosses Kazakhstan and continues to Iran or Turkey (via the Caucasus) with a possible extension to Europe[1].

Next to these "Eurasian" roads there are three corridors:

China-Pakistan, China-Laos-Thailand, Bangladesh-China-India-Myanmar, leading to ports that are the starting point of maritime roads crossing the Indian Ocean and going along the African continent to Europe.

The Eurasian Belt and the rail transport challenge

At the end of the 2000s[2], chartered trains arranged by car manufacturers and electronics companies started rail transport between China and Europe. It rose very rapidly in the 2010s: from 17 convoys in 2011, to 80 in 2013, 815 in 2015[3] and nearly 5,000 in 2018 (some larger estimates include traffic directed to Russia). The number of containers transported by rail increased a hundredfold to reach 280,000 units in 2018.

Measured in volume (number of containers), railway transport accounts for 1.3 % of China Europe trade[4] in 2016, behind aircraft (1.9 %) and maritime traffic (95 %). In value terms, these shares are respectively 2 %, 28% and 70%. This traffic is unbalanced as trains going to Europe are full when half is loaded back to China. These trains carry car parts, electronic components, durable goods and steel products.

Until 2006, railway transport between China and Europe was slower and more expensive than sea transport. The reduction of transport time, from 35 to 16 days, which led to the increase of rail’s share is explained by progress in operation management (including transshipment) and faster train speeds. They reach 100 km / h in Russia instead of 60 km / h), while at the same time, to limit their carbon emissions, ships slowed their speed. The rise of the Railways is also due to the support by the western and central Chinese provinces-Chongqing towards Duisburg (Germany), Wuhan towards Lyon, Yiwu towards London. In order to circumvent the bureaucracy of Chinese railways, the state entrusted the management of these lines to operators originated from these provinces, which compete to become a gateway to Europe. They offer subsidies – larger for transport from Europe than to words Europe – which cover the additional cost of Chinese rail transport[5] and average $ 4,000 per 40-foot container, or $ 600 million per year for all provinces. In 2018, the Chinese government asked provinces to reduce these subsidies, which should account for no more than half of the (domestic) cost of transportation and should be eliminated by 2020. Chinese provinces have also invested in improving railway stations and building dry ports, such as Khorgos on the border between China and Kazakhstan.

While railway is twice as fast as maritime transport, its cost is three times that of shipping (the subsidy granted by Chinese Provinces reduce the cost by half for the shipper). Taking into account the cost of working capital, the difference is reduced to 32% for a container worth 750,000 dollars (transported in 20 days by rail) and 6% for a container worth 1.5 million – filled with laptops for example. In addition, non-quantifiable costs such as better regularity and better safety, must be taken into account, knowing that these factors which differ according to the shippers may be decisive for the choice of a mode of transport.

|

40 ft container carrying goods valued at $ 750,000 by rail. |

By rail |

By boat |

|

Duration in days |

20 |

40 |

|

Price charged to the shipper |

4,000** |

2,000 |

|

Financial charges (working capital*) |

822 |

1,644 |

|

Cost for the shipper |

4,822 |

3,644 |

** This cost is due to the subsidy provided by the Chinese provinces, which would average $ 4,000 per container.

Sources: based on data from Jacob Jakowski op.cit. and Xavier Wanderpepen[6]

The railway uses the network inherited from the Soviet era, to which were added connections built by Kazakhstan in the early 1990s. In the framework of the BRI, the track improvements[7] allowed a reorganization of the transport chain which led to a reduction in transport time[8]. These changes would not have been possible without cooperation between the railway companies of the different Eurasian countries.

Will rail replace maritime transport? Its adoption by new shippers as well as the introduction of slightly faster trains carrying more containers (80 instead of 60) could make up for the gradual elimination of Chinese subsidies. The traffic between China and Europe was 14 trains per day in 2018. The International Union of Railways (IUR) plans 24 trains per day in 2020 and by 2027 as traffic could reach 54 trains per day, it could carry 10% of the freight China Europe in volume[9] and probably 15% in value.

In the medium term, rail will continue to gain market shares over air and, without replacing sea transport, it will expand the range of choice of Chinese and European shippers while allowing Chinese logistics companies to enter the world market. Technological improvements (connected cars, rail automation) will reduce transport time; in the longer term, the adoption outside Europe of cleaner electricity[10] and carbon-based pricing could increase the advantage of rail transport between Europe and China.

Corridors

By developing the Belt, China wants to open up western provinces and improve connectivity within Eurasia. The focus of the South and South-East Asian corridors is more regional : an easier access to the Indian Ocean, Yunnan development and circumventing the strategically unstable South China Sea.

Linking the belt to the maritime Route, the CESP is the most ambitious BRI project . Between 1966 and 1978, Chinese and Pakistanis built the Karakoram route which, crossing a pass at 5,600 meters and a territory claimed by India (Kashmir), leads to Islamabad. In 2006 China built the Port of Gwadar in Balochistan, a province agitated by irredentist movements. Proposed in 2006, the completion of the energy and trade corridor should make this secondary port (5% of Pakistan's maritime trade) a major transit port to China. Covering 3000 kilometers, the CESP includes railways, pipelines and optical cables, power stations and special economic Zones (SEZs). The corridor was malfunctioning when in 2013 its management was entrusted to the Chinese Overseas Ports Holding Company for 43 years. The investment (equivalent to 19 % of Pakistan'S GDP in 2016) would reach $ 55 billion over the next ten years[11] and could make Gwadar a transit port equivalent to that of Shenzen.

The Indo-Chinese corridor: the integration of South-East Asia

The China-Indochina corridor connects the outlying Chinese province of Yunnan to Southeast Asia. Work on the Kunming-Boten-Luang Prabang-Vientiane line, which has been repeatedly announced and postponed since 2010, began in early 2017 and progresses very rapidly on very rough terrain (40% of tunnels and bridges). It[12] represents a huge investment for Laos (45 % of GDP) and it will connect with the railway linking the Laotian border to the Port of Map Ta Phut on the Gulf of Siam (a 2017 Memorandum of Understanding (MoU) between China and Thailand). Beyond the situation became since the victory of Mahatir in Malaysia: the new government asked for a review of the projects signed by the Government of Najib, including the High-Speed Line between Kuala Lumpur and Singapore.

This corridor poses a major problem for Vietnam[13] which has over-invested in the construction of deep-sea ports which operate at only 20% of their capacity. Moreover, the conflicts over the division of territorial waters and the opposition of part of the Vietnamese population to Chinese involvement put the government in a difficult position as it needs Chinese freight for its development.

Projected as early as 1999, the BCIM corridor linking Kunming to Kolkota in India, 2,800 kilometers via Myanmar and Bangladesh, involves the construction of a road and a railway. In the absence of an international agreement this corridor is the least developed, however, the China Myanmar Economic corridor, which could serve as a link to the BCIM, is progressing. China signed an agreement for the construction of a railway line between Kunming and the Burmese port of Kyaukphyu on the Bay of Bengal which will be added to the oil and gas pipeline in operation since 2013.

Sea routes

A few months after presenting the land-based version of the BRI in Astana, Xi Jinping announced at the Asia-Africa Summit in Jakarta plans for maritime routes . Several ports along these routes are part of the “pearl necklace”[14] that China began to build before the announcement of the BRI project.

In this context, several African countries joined the BRI and China financed the railways between Djibouti – where the Chinese navy built a naval base – and Addis Ababa (Ethiopia), Mombasa and Nairobi (Kenya) – and a port in Bagamoyo (Tanzania) which could become the largest in East Africa. Chinese firms are involved in the management of African port facilities.

Finally, a growing number of countries distant from these roads joined the BRI : in North Africa (Algeria, Morocco), West Africa (Ghana, Senegal), South America (Ecuador, Peru, Chile) and the South Pacific (New Zealand, Tonga, Vanuatu). All in all, the scale of these projects inevitably raises the question of financing and its counterparts, which we will discuss in the following notes.

[1] The improvement of the railway between Baku and the Black Sea, the line to Iran, a new route between Kashgar and Andijan would aim less to improve connectivity between China, Iran and Turkey that can be connected by sea, than to strengthen a credible alternative to the route through Russia.

[2] In 2008, Foxconn organized a first train from Shenzhen, in 2009, DB Schenker, RZD (Russian) and China Railway launched a weekly service between Duisburg and Shanghai (where SAIC is located linked to Volkswagen) ; the Polish Hatrans developed a similar service between Lodz (Dell) and Chengdu and since 2011, HP uses a service between Chongqing and Duisburg.

[3] Jacub Jakowski and others. 2018. The silk railroad, The Eu, China rail connections: background, actors, interests, Center for Eastern Studies, Warsaw, Poland p. 29.

[4] Eurostat Data for 2017.

[5] Chinese railways have made a considerable investment in the construction of 25,000 km of high-speed (passenger) lines.

[6] Xavier Wanderpepen. 2017. The Silk road, geopolitical issues of the rail freight international in Eurasia. The International Review n° 107, Fall.

[7] Prior to the launch of the BRI, Kazakhstan invested $ 3.3 billion in the upgrading of Railways and the construction of the Dry Port of Khorgos on the Chinese border.

[8] The modification of the methods of loading and unloading containers by placing two trains side by side on two tracks with different gauge and by sliding the containers from one wagon to another, would have significantly reduced the duration of the transhipment.

[9] Xavier Wanderpepen op. cit.

[10] According to the data of ADEME, the carbon emission for the transport of one-ton km is 29 grams by sea, 20 grams by rail with diesel traction (little used), 2 grams by rail with electric traction in France and 10 grams outside France where electricity is more often produced by coal-fired power plants.

[11] This amount is divided into $ 17.7 billion for the Energy Sector, $ 5 billion for infrastructure and $ 25.4 billion for projects in Special Economic Zones. Source IMF article IV Pakistan July 2017.

[12] The cost of the Boten-Vientiane project is nearly $ 6 billion; Laos and China have agreed to share 30% -70 %. This line will be joined by a motorway which could be inaugurated in 2021.

[13] Nathalie Fau. 2015. La maritimisation de l’économie vietnamienne : un facteur exacerbant les conflits entre le Viêt Nam et la Chine en mer de Chine méridionale ? Hérodote n° 127, pages 39 à 55.

[14] The so-called "pearl necklace" strategy is the expression coined in 2004 by a report by Booze Allen Hamilton for the Defense Secretariat of the United States to report on the initiatives of the Chinese navy, which built a network of military ports and logistical support around the Indian subcontinent and beyond. Among these ports there is one of Sihanoukville in Cambodia, Kyaukpyu and Sittwe in Myanmar, Chittagong in Bangladesh, Hambantota in Sri Lanka, Gwadar in Pakistan, Doraleh and Obock in Djibouti, Port Sudan in Sudan.

Jean-Raphaël Chaponnière is an associate researcher at Asia Centre and the Asia21

|

Retrouvez plus d'information sur le blog du CEPII. © CEPII, Reproduction strictement interdite. Le blog du CEPII, ISSN: 2270-2571 |

|||

|